# Strategy Setup

Tips

- The content of this trading strategy is not an investment advice. It is for learning purposes only.

# Strategy Introduction

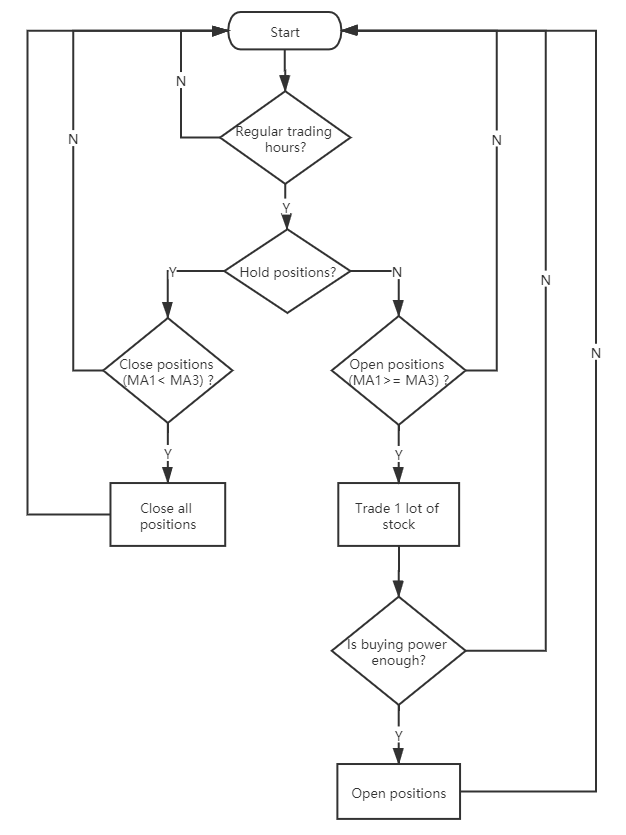

Contruct a Double Moving Averaging Strategy.

That is, using the 1 minute candlestick of an underlying stock, to calculate two moving averages of different periods, MA1 and MA3. The values of MA1 and MA3 are tracked to determine the timing of buying and selling.

When MA1 >= MA3, the underlying stock is judged to be strong and the market is considered to be a bull market, which shows a long signal.

When MA1 < MA3, the underlying stock is judged to be weak and the market is considered to be a bear market, which shows a short signal.

# Flow Chart

# Code Sample

- Example

from futu import *

############################ Global Variables ############################

FUTU_OPEND_ADDRESS = '127.0.0.1' # OpenD listening address

FUTU_OPEND_PORT = 11111 # OpenD listening port

TRADING_ENVIRONMENT = TrdEnv.SIMULATE # Trading environment: REAL / SIMULATE

TRADING_MARKET = TrdMarket.HK # Transaction market authority, used to filter accounts

TRADING_PWD = '123456' # Trading password, used to unlock trading for real trading environment

TRADING_PERIOD = KLType.K_1M # Underlying trading time period

TRADING_SECURITY = 'HK.00700' # Underlying trading security code

FAST_MOVING_AVERAGE = 1 # Parameter for fast moving average

SLOW_MOVING_AVERAGE = 3 # Parameter for slow moving average

quote_context = OpenQuoteContext(host=FUTU_OPEND_ADDRESS, port=FUTU_OPEND_PORT) # Quotation context

trade_context = OpenSecTradeContext(filter_trdmarket=TRADING_MARKET, host=FUTU_OPEND_ADDRESS, port=FUTU_OPEND_PORT, security_firm=SecurityFirm.FUTUSECURITIES) # Trading context. It must be consistent with the underlying varieties.

# Unlock trade

def unlock_trade():

if TRADING_ENVIRONMENT == TrdEnv.REAL:

ret, data = trade_context.unlock_trade(TRADING_PWD) # Live trading requires unlocking first; if using the GUI version of OpenD, skip this step and unlock manually by clicking the Unlock button on the UI

if ret != RET_OK:

print('Unlock trade failed: ', data)

return False

print('Unlock Trade success!')

return True

# Check if it is regular trading time for underlying security

def is_normal_trading_time(code):

ret, data = quote_context.get_market_state([code])

if ret != RET_OK:

print('Get market state failed: ', data)

return False

market_state = data['market_state'][0]

'''

MarketState.MORNING HK and A-share morning

MarketState.AFTERNOON HK and A-share afternoon, US opening hours

MarketState.FUTURE_DAY_OPEN HK, SG, JP futures day market open

MarketState.FUTURE_OPEN US futures open

MarketState.FUTURE_BREAK_OVER Trading hours of U.S. futures after break

MarketState.NIGHT_OPEN HK, SG, JP futures night market open

'''

if market_state == MarketState.MORNING or \

market_state == MarketState.AFTERNOON or \

market_state == MarketState.FUTURE_DAY_OPEN or \

market_state == MarketState.FUTURE_OPEN or \

market_state == MarketState.FUTURE_BREAK_OVER or \

market_state == MarketState.NIGHT_OPEN:

return True

print('It is not regular trading hours.')

return False

# Get positions

def get_holding_position(code):

holding_position = 0

ret, data = trade_context.position_list_query(code=code, trd_env=TRADING_ENVIRONMENT)

if ret != RET_OK:

print('Get holding position failed:', data)

return None

else:

for qty in data['qty'].values.tolist():

holding_position += qty

print('[Holidng Position Status] The holidng position quantity of {} is:{}'.format(TRADING_SECURITY, holding_position))

return holding_position

# Query for candlesticks, calculate moving average value and judge bull or bear

def calculate_bull_bear(code, fast_param, slow_param):

if fast_param <= 0 or slow_param <= 0:

return 0

if fast_param > slow_param:

return calculate_bull_bear(code, slow_param, fast_param)

ret, data = quote_context.get_cur_kline(code=code, num=slow_param + 1, ktype=TRADING_PERIOD)

if ret != RET_OK:

print('Get candlestick value failed: ', data)

return 0

candlestick_list = data['close'].values.tolist()[::-1]

fast_value = None

slow_value = None

if len(candlestick_list) > fast_param:

fast_value = sum(candlestick_list[1: fast_param + 1]) / fast_param

if len(candlestick_list) > slow_param:

slow_value = sum(candlestick_list[1: slow_param + 1]) / slow_param

if fast_value is None or slow_value is None:

return 0

return 1 if fast_value >= slow_value else -1

# Get ask1 and bid1 from order book

def get_ask_and_bid(code):

ret, data = quote_context.get_order_book(code, num=1)

if ret != RET_OK:

print('Get order book failed: ', data)

return None, None

return data['Ask'][0][0], data['Bid'][0][0]

# Open long positions

def open_position(code):

# Get order book data

ask, bid = get_ask_and_bid(code)

# Get quantity

open_quantity = calculate_quantity()

# Check whether buying power is enough

if is_valid_quantity(TRADING_SECURITY, open_quantity, ask):

# Place order

ret, data = trade_context.place_order(price=ask, qty=open_quantity, code=code, trd_side=TrdSide.BUY,

order_type=OrderType.NORMAL, trd_env=TRADING_ENVIRONMENT,

remark='moving_average_strategy')

if ret != RET_OK:

print('Open position failed: ', data)

else:

print('Maximum quantity that can be bought less than transaction quantity.')

# Close position

def close_position(code, quantity):

# Get order book data

ask, bid = get_ask_and_bid(code)

# Check quantity

if quantity == 0:

print('Invalid order quantity.')

return False

# Close position

ret, data = trade_context.place_order(price=bid, qty=quantity, code=code, trd_side=TrdSide.SELL,

order_type=OrderType.NORMAL, trd_env=TRADING_ENVIRONMENT, remark='moving_average_strategy')

if ret != RET_OK:

print('Close position failed: ', data)

return False

return True

# Calculate order quantity

def calculate_quantity():

price_quantity = 0

# Use minimum lot size

ret, data = quote_context.get_market_snapshot([TRADING_SECURITY])

if ret != RET_OK:

print('Get market snapshot failed: ', data)

return price_quantity

price_quantity = data['lot_size'][0]

return price_quantity

# Check the buying power is enough for the quantity

def is_valid_quantity(code, quantity, price):

ret, data = trade_context.acctradinginfo_query(order_type=OrderType.NORMAL, code=code, price=price,

trd_env=TRADING_ENVIRONMENT)

if ret != RET_OK:

print('Get max long/short quantity failed: ', data)

return False

max_can_buy = data['max_cash_buy'][0]

max_can_sell = data['max_sell_short'][0]

if quantity > 0:

return quantity < max_can_buy

elif quantity < 0:

return abs(quantity) < max_can_sell

else:

return False

# Show order status

def show_order_status(data):

order_status = data['order_status'][0]

order_info = dict()

order_info['Code'] = data['code'][0]

order_info['Price'] = data['price'][0]

order_info['TradeSide'] = data['trd_side'][0]

order_info['Quantity'] = data['qty'][0]

print('[OrderStatus]', order_status, order_info)

############################ Fill in the functions below to finish your trading strategy ############################

# Strategy initialization. Run once when the strategy starts

def on_init():

# unlock trade (no need to unlock for paper trading)

if not unlock_trade():

return False

print('************ Strategy Starts ***********')

return True

# Run once for each tick. You can write the main logic of the strategy here

def on_tick():

pass

# Run once for each new candlestick. You can write the main logic of the strategy here

def on_bar_open():

# Print seperate line

print('*****************************************')

# Only trade during regular trading hours

if not is_normal_trading_time(TRADING_SECURITY):

return

# Query for candlesticks, and calculate moving average value

bull_or_bear = calculate_bull_bear(TRADING_SECURITY, FAST_MOVING_AVERAGE, SLOW_MOVING_AVERAGE)

# Get positions

holding_position = get_holding_position(TRADING_SECURITY)

# Trading signals

if holding_position == 0:

if bull_or_bear == 1:

print('[Signal] Long signal. Open long positions.')

open_position(TRADING_SECURITY)

else:

print('[Signal] Short signal. Do not open short positions.')

elif holding_position > 0:

if bull_or_bear == -1:

print('[Signal] Short signal. Close positions.')

close_position(TRADING_SECURITY, holding_position)

else:

print('[Signal] Long signal. Do not add positions.')

# Run once when an order is filled

def on_fill(data):

pass

# Run once when the status of an order changes

def on_order_status(data):

if data['code'][0] == TRADING_SECURITY:

show_order_status(data)

############################### Framework code, which can be ignored ###############################

class OnTickClass(TickerHandlerBase):

def on_recv_rsp(self, rsp_pb):

on_tick()

class OnBarClass(CurKlineHandlerBase):

last_time = None

def on_recv_rsp(self, rsp_pb):

ret_code, data = super(OnBarClass, self).on_recv_rsp(rsp_pb)

if ret_code == RET_OK:

cur_time = data['time_key'][0]

if cur_time != self.last_time and data['k_type'][0] == TRADING_PERIOD:

if self.last_time is not None:

on_bar_open()

self.last_time = cur_time

class OnOrderClass(TradeOrderHandlerBase):

def on_recv_rsp(self, rsp_pb):

ret, data = super(OnOrderClass, self).on_recv_rsp(rsp_pb)

if ret == RET_OK:

on_order_status( data)

class OnFillClass(TradeDealHandlerBase):

def on_recv_rsp(self, rsp_pb):

ret, data = super(OnFillClass, self).on_recv_rsp(rsp_pb)

if ret == RET_OK:

on_fill(data)

# Main function

if __name__ == '__main__':

# Strategy initialization

if not on_init():

print('Strategy initialization failed, exit script!')

quote_context.close()

trade_context.close()

else:

# Set up callback functions

quote_context.set_handler(OnTickClass())

quote_context.set_handler(OnBarClass())

trade_context.set_handler(OnOrderClass())

trade_context.set_handler(OnFillClass())

# Subscribe tick-by-tick, candlestick and order book of the underlying trading security

quote_context.subscribe(code_list=[TRADING_SECURITY], subtype_list=[SubType.TICKER, SubType.ORDER_BOOK, TRADING_PERIOD])

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

100

101

102

103

104

105

106

107

108

109

110

111

112

113

114

115

116

117

118

119

120

121

122

123

124

125

126

127

128

129

130

131

132

133

134

135

136

137

138

139

140

141

142

143

144

145

146

147

148

149

150

151

152

153

154

155

156

157

158

159

160

161

162

163

164

165

166

167

168

169

170

171

172

173

174

175

176

177

178

179

180

181

182

183

184

185

186

187

188

189

190

191

192

193

194

195

196

197

198

199

200

201

202

203

204

205

206

207

208

209

210

211

212

213

214

215

216

217

218

219

220

221

222

223

224

225

226

227

228

229

230

231

232

233

234

235

236

237

238

239

240

241

242

243

244

245

246

247

248

249

250

251

252

253

254

255

256

257

258

259

260

261

262

263

264

265

266

267

268

269

270

271

272

273

274

275

276

277

278

279

280

281

282

283

284

285

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

100

101

102

103

104

105

106

107

108

109

110

111

112

113

114

115

116

117

118

119

120

121

122

123

124

125

126

127

128

129

130

131

132

133

134

135

136

137

138

139

140

141

142

143

144

145

146

147

148

149

150

151

152

153

154

155

156

157

158

159

160

161

162

163

164

165

166

167

168

169

170

171

172

173

174

175

176

177

178

179

180

181

182

183

184

185

186

187

188

189

190

191

192

193

194

195

196

197

198

199

200

201

202

203

204

205

206

207

208

209

210

211

212

213

214

215

216

217

218

219

220

221

222

223

224

225

226

227

228

229

230

231

232

233

234

235

236

237

238

239

240

241

242

243

244

245

246

247

248

249

250

251

252

253

254

255

256

257

258

259

260

261

262

263

264

265

266

267

268

269

270

271

272

273

274

275

276

277

278

279

280

281

282

283

284

285

- Output

************ Strategy Starts ***********

*****************************************

[Position] The position of HK.00700 is 0

[Signal] Long signal. Open long positions.

[OrderStatus] SUBMITTING {'Code': 'HK.00700', 'Price': 597.5, 'TradeSide': 'BUY', 'Quantity': 100.0}

[OrderStatus] SUBMITTED {'Code': 'HK.00700', 'Price': 597.5, 'TradeSide': 'BUY', 'Quantity': 100.0}

[OrderStatus] FILLED_ALL {'Code': 'HK.00700', 'Price': 597.5, 'TradeSide': 'BUY', 'Quantity': 100.0}

*****************************************

[Position] The position of HK.00700 is 100.0

[Signal] Short signal. Close positions.

[OrderStatus] SUBMITTING {'Code': 'HK.00700', 'Price': 596.5, 'TradeSide': 'SELL', 'Quantity': 100.0}

[OrderStatus] SUBMITTED {'Code': 'HK.00700', 'Price': 596.5, 'TradeSide': 'SELL', 'Quantity': 100.0}

[OrderStatus] FILLED_ALL {'Code': 'HK.00700', 'Price': 596.5, 'TradeSide': 'SELL', 'Quantity': 100.0}

1

2

3

4

5

6

7

8

9

10

11

12

13

2

3

4

5

6

7

8

9

10

11

12

13